Financial Road Map

One of the easiest and most effective ways to improve your financial situation is to create a Financial Plan. And, before you ask, YES there is room for improvement with your financial situation. Regardless of who is reading this and what your current financial and economic standings are, there is always room for improvement.

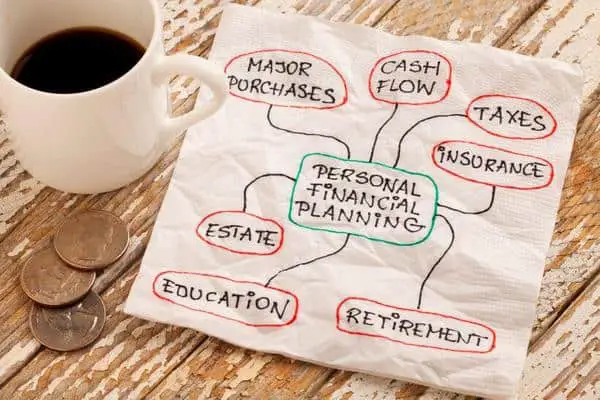

What is a Financial Plan?

A financial plan is a comprehensive view of all of your current finances, as well as the strategies you’ve set to achieve your financial goals. To create a financial plan that will work for you, you will need to include any and all possible details about your finances.

These financial details can include your cash flow or income(s), deposits, savings, investments, insurance, any current debt, and anything else that has to do with your overall finances. And we mean anything else.

Financial planning is key to determining your financial goals and setting up ways to achieve these goals. Whether they are short-term or long-term, creating a budget and a financial plan will help you stay on top of your spending habits. In addition, it helps you to get out of debt efficiently, meet any long-term or short-term savings and investment goals.

Financial planning is not only for the rich or wealthy: Creating a financial roadmap for you and your household’s financial future should be done by everyone. You can create a financial plan yourself with a pen and paper, or you can get help from a financial advisor.

Benefits of Creating a Financial Plan

Financial independence and future success go hand in hand with having a carefully curated financial plan. By developing your own financial plan you can not only understand how your future financial health will be affected but also get a comprehensive view of your current financial needs.

A financial plan can directly impact many aspects of your life, not just the parts that are centered around money. By that logic, it’s safe to say that a proper financial plan can improve your quality of life overall.

Here are seven reasons why creating a financial plan can benefit you both now and in the future:

- Find Financial Weak Points

Starting on a journey and not knowing how to get to your destination is essentially what you are doing with your finances when you don’t have a financial plan. Laying out all of your current finances and future goals in a concise way. One other thing, it will give you an overview of your current financial standing.

From there you will be able to see what areas are lacking or need more support, and you can change your plan accordingly. Once you have defined your financial weak points and have identified your financial goals. Consequently, you will know what areas you need to focus on the most.

- Motivation For Financial Improvement

There will undoubtedly be uncertainty with both your finances and the future, but this doesn’t have to be a bad thing. By painting a clear picture of your financial situation and identifying weak points. As a result, you would have a clear-cut reason to make positive changes.

A financial plan will provide a road map or a sense of direction for your finances. It helps you to measure results as you progress and can keep you motivated upon reaching certain milestones. Because results from a financial plan aren’t exactly immediate, it’s good to attain mini-goals along the way to keep you motivated.

- Ideal Goals vs. Realistic Goals

While working through your financial plan you may end up realizing that your current wants or goals are unattainable for the time being. That’s okay! . It’s very important to have realistic goals and expectations.

In fact, it may take some trial and error to create the perfect financial plan and to realize attainable goals. Make proper adjustments as needed to get it back in line. Having an accurate financial plan will allow you to compare your goals and set realistic ways to attain them. Admittedly, it’s a fantastic way to ensure you are on track, and compare your goals to your financial activities and adjust as needed.

- Guides Your Actions & Decisions

Following a financial plan won’t always be easy. In fact there will be plenty of difficult times and these scenarios will require a sense of discipline and commitment.

A financial plan will provide you with the steps you will need to take in order to reach your goals. Your future actions and decisions will be laid out for you. Almost like a road map, all based around your financial plan.

- Build Wealth & Confidence

Creating a financial plan will provide you with the confidence needed to keep moving forward to achieve your financial goals. Being able to review and see the positive progress in managing your money can build confidence.

Unquestionably, if it’s followed correctly it will show positive growth in your wealth creation. A clear, reflection that your financial plan is working successfully.

If you haven’t realized it yet, feeling good about your finances. Also, it can directly cross over to feeling good about other areas of your life. Since money is a commodity that revolves around almost all aspects of your daily life. Feeling successful with your money can lead to confidence in other areas of your daily living.

- Make The Most Of Money

One of the main goals of a financial plan is to be highly efficient with your money. Through budgeting, saving, and wisely investing. While minimizing expenditures and debts.

Think about a large corporation. Do they just take whatever revenue comes in, and spend it on whatever they want? Or do they obsessively track every single penny that comes in, and dictate rules about every single penny that goes back out?

- Emotional & Health Benefits

You’ve probably heard the saying that ‘health is wealth’ and that is extremely true. Worrying about money and finances can create unnecessary strain on your day-to-day lives and relationships.

This is where a financial plan will add a bonus to areas of your life that are not focused on money. Having a plan that manages your personal finances is extremely beneficial for your health.

If you have a plan on how to spend and save your money. You will, in turn, be less stressed and anxious when it comes to thinking about the future. Many people would be in a terrible position financially if an unexpected expense popped up — medical bills, car repair, home repair, etc.. — this can cause tremendous amounts of stress and anxiety.

Meanwhile, someone who has better control over their finances will not be as anxious about what the future holds. This lack of anxiety and stress will work wonders for your overall health and mental wellbeing.

Related: A Comprehensive Financial Planning Process in 6 Steps

Components of a Financial Plan

Every good plan is like a puzzle. You need to have the right pieces. And those pieces need to fit into their respective spots perfectly. The components of a financial plan encompass all of the pieces needed to put this puzzle together. Of course, your puzzle may look different than the puzzle that someone else is putting together.

- Personal Financial Health

- Balance Sheet – Also known as a Statement of Financial Position, a balance sheet will help you calculate your net worth. It’s essentially a list of all of your assets and liabilities and it will change as you work to improve your overall finances.

- Cash Flow Statement – You want to map out every single dollar that comes in as income to you, and where that money comes from. You then want to list every expense that occurs regularly or on a recurring basis.

- Financial Risks & Insurance

- Health Insurance (Medical, Dental, and Vision)

- Life Insurance

- Long-Term & Short-Term Disability

- Liability Insurance (this is especially important depending on your profession)

- Long-Term Care Insurance (should something happen to you, you don’t want your entire net worth to be wasted away on something that insurance would have covered)

- Investment Management

- Planning for Retirement

- Tax Planning

- Estate Planning

- Education Planning

The overall state of your finances is your Financial Health. There is no set of rules that can be used to determine someone’s financial health as everybody has different economic standings, and different incomes. Also, different short-term and long-term goals.

There are many dimensions to your financial health, many of which are covered throughout this list of components. Below are the two main aspects needed to get an idea of your financial health:

When it comes down to your money, risks can come in many different shapes and sizes. Whether you are trying to figure out how long your money will last, how you will pay for future expenses.Usually, how to cover long-term care costs, your financial plan should give you an idea of any potential risks you face.

The goal is to find those risks early enough and be able to create a plan to move forward keeping those risks in mind.

Most people typically overlook their greatest asset in regards to their finances, and that is their ability to earn income. Since we don’t have a magic ball that will tell us what the future holds. It’s important to keep in mind future possibilities that can affect your income.

These can include an on-the-job accident that keeps you from working. As well as, a loved one dying and you having to take a leave of absence from your job, your company closing down (like many did for Covid-19), and many other possibilities.

By mapping out any potential risks that can affect your finance. Obviously, you are able to see which insurance products would be great at mitigating these risks. At the very least you should be evaluating your:

When creating your financial plan you should also take into account how much risk you are willing to take in regards to investing. In the investment community, this is known as your Risk Tolerance. You can find risk questionnaires online that can accurately assess your tolerance for risk. As a result, you will invest based on the risk-return principle.

If you currently have investments, a financial plan will analyze how your current investments are stacking up compared to your risk. Your plan will also show you how proper asset allocation can provide a clear path to wealth and have your investments work for you.

Sitting down with your financial advisor you will be able to create a plan that can serve as a benchmark to follow for any future investing ventures.

A 25-year-old who is just hitting the workforce has got plenty of wiggle room to make some risky stock investments. Since they have got decades to make up for any losses. Someone who is a few years away from retirement cannot afford to be so risky with their money. As they will need it to survive and maintain their ideal lifestyle in retirement.

Related:How to Save Money for a House in 17 Sure-fire Ways

It’s never too early to start planning for retirement. A fantastic financial plan will show you roughly the expected retirement finances after leaving your career.

Because of the power of Compound Interest. Planning for retirement as early as possible can make the difference between retiring with a 6-figure retirement fund, or retiring as a multi-millionaire. Take a look at the Investor.gov Compound Interest Calculator to see why starting sooner is so important.

Once you have created a financial plan with retirement goals in mind. Reveals the amount of money you are currently saving on a tax-deferred basis to continuously support your lifestyle. It will also show you any areas where you can save extra money to put towards your retirement.

Essentially, all aspects of your money should be accounted for, and if you have extra. Adding it to your retirement fund can prove to be extremely beneficial in the long run.

Related:Understanding How To Invest In Mutual Funds, Risks and Benefits For A Beginners

You can’t forget to include Uncle Sam as your other financial partner when planning out your finances. A good plan will show you any compounding benefits of tax deferral options and how those can play out in the future.

Whether you are using traditional IRAs, Roth IRAs, 401Ks, (Tax-free saving account or RRSP in Canada), or any other qualified plans. Be aware of any tax-free or tax-deferred withdrawals when you reach retirement. Overall, your financial plan goals with regards to tax planning will eliminate any unnecessary tax drag. While also preserving any assets and net income that will affect your long-term wealth.

While it may be more difficult to think about right now, a lack of a clear financial plan can lead to a loss of large fortunes and assets, which is why including estate planning in your financial plan is so important.

Do you know the current and future amounts of federal and state estate (Federal and provincial in Canada)taxes that you are facing? That is the purpose of a financial plan because it will outline how much tax you will be paying right now and in the future. It should also show any future estate taxes you will owe based on the projected growth of your estate.

Planning for future education expenses can be scary as tuition rates continue to climb. However, a good financial plan should allow ample time to save as much money as possible to make those scenarios easier to handle financially. But your education is amazing. It’s an investment in yourself and a great way to ensure you bring in more income later in life.

Education planning can be done with regards to you personally, or to any of your children or dependents. A great way to save up for your little ones’ education is by using a government-backed 529 plan. 529 plans come in two types, either a prepaid tuition plan or a college savings plan. Be sure to consider those options whilst doing your education planning.

In Canada, you can open a Registered Education Saving account(RESP). A registered education savings plan (RESP)is an investment account available to parents and grandparents to save for their children’s post-secondary education. The main advantages of RESPs are access to the Canada Education Savings Grant (CESG) and as well as a vehicle for generating tax-deferred income.

How To Create A Financial Plan

By now you should have a pretty good understanding of why everyone should be creating a financial plan, and what components are involved with creating a financial plan. But how exactly do you make one?

Whenever you fill out your tax forms for a new job, those tax forms always look the same. They look the same no matter which job you’re working at and it’s the same exact form for all of the employees involved.

A financial plan will NOT be the same as that for everyone. There isn’t some magical financial plan form like there is with taxes. A financial plan is unique to you and will look different for everybody. Your financial plan might be written in pencil on a notebook, whereas another reader might head over to their financial advisor to create a professional-looking plan in Excel.

Here’s the thing: It’s okay if your actual plan doesn’t look professional. The most important part about all of this is getting you to take the first step of sitting down and going through your finances. It’s probably going to be messy and confusing the first time, and that’s okay!

Ideally, a financial plan is created in tandem with a Certified Financial Planner (CFP). But if you can’t afford or don’t have access to one, then writing out your own plan is better than nothing!

- Establish Professional Relationships

- Determine What You Want to Achieve & Define Your Goals

- Review Your Personal Financial Data

- Evaluate Your Financial Situation

- How much you have in liquid assets (cash, bank accounts, CDs, etc)

- The value of your investment portfolio

- The size(s) of your retirement account(s)

- The cash-value of any life insurance plans

- How much debt you owe

- Homeowners: how much you owe on your mortgage and how much equity is currently in you home

- Implement Your Financial Plan

- Review Your Financial Plan Periodically

The process of developing a financial plan is ideally a collaborative process between an individual and their CFP or CPA. If you have the means to have your financial plan created professionally, then it can make all the difference in the world.

Again, working with a professional is ideal, but it is far from mandatory. If you’re going to try to tackle this by yourself then you may want to use third-party apps that will help you track your incomes, debts, and expenditures.

Short-term and long-term goals are one of the most important aspects of creating a financial plan. Without these goals, you have nothing to strive for and you have no motivating factors behind improving your financial situation.

Try to be as specific as possible with your goals. “I want to be rich!” doesn’t exactly give you something to shoot for. “I want to retire with $3 Million in my retirement accounts when I turn 62.” is a much more specific and attainable long-term goal.

Short-term goals are just as helpful. You may want to save up for the down payment on a new home 2 years from now. Or maybe you’d like to have all of your high-interest debt paid off in 18 months. Very specific short-term goals will offer small rewards along the path to achieving your long-term goals.

Before you can make changes to your financial situation. First, have a very good understanding of how much money you have coming in and where every single penny is going out to. This goes back to the Financial Health (cash flow and income statements, assets, and liabilities) component that we mentioned earlier. Every single dollar should be accounted for.

A Certified Financial Planner will be able to go through all of your bank and accounting statements. And, again, those who are creating a financial statement on their own could greatly benefit from some of the apps we mentioned above in Step 1.

Now that you’ve accounted for all money coming in, and all money going out, you can evaluate your current financial situation. This is going to look much different than your income and expenditures or obligations above. Your evaluation should include:

Now that you have created your financial plan. It is time to put it to work! While this may sound like a simple step. many people find this one to be the more difficult step in financial planning.

A successful plan will not work without determination and discipline to put it into action. It’s one thing to get started on creating your financial plan. But putting that plan to work is an entirely different ballgame. Humans are creatures of habit and we love feeding into that reward section of our brain.

It takes a lot of discipline to put a certain fraction of your income into an investment account that you won’t touch for decades from now. It takes a lot of discipline to not impulsively buy those things that make us happy.

But following your plan so that you can meet your short-term and long-term goals is arguably one of the best feelings in the world. Especially, once you’ve finally started to see progress and success!

Your financial plan will only work as long as you keep up with it. This is why going back periodically to check how your finances are measuring up with your plan is essential. Compare your finances now with how they were before. Revisit your goals to see if anything has changed.

Throughout your life, there will be changes to your personal, social, and economic status which may require some additional revisions to your original financial plan. A great financial plan will grow and change with you, as your life does.

Top 4 Reasons Why Financial Planning Helps You Increase Your Net Worth

- Get out of debt faster: With financial planning, you are constantly looking at your money and how it is being allocated. Utilizing a financial plan will allow you to see what areas you can shred spending, and put that newly-found money towards making larger debt payments.

Even though you may have no trouble making your suggested monthly payments, paying more each month can help to quickly wear away at the original principal amount that you owe.

- Be able to budget to trim unnecessary spending: Just like creating a budget, financial planning can show you what percentage of your money is going where. In addition, you can make this as specific as you’d like. When looking over your financial plan you can see where there is a waste.

This can be a gym membership you haven’t used in months, a streaming service you don’t watch, or even seeing that you spend entirely too much money eating out each week. The point of a financial plan is to see what you are currently doing with your finances, and how you can adjust them to achieve your goals.

- Help you grow your investments and retirement accounts: Investing as much as possible, as early as possible, is one of the easiest ways to guarantee a happy retirement. By taking a clear-cut look at your finances using a financial plan. It’s easy to identify extra ways that will allow you to contribute to your investments or retirement accounts more. Determine your risk tolerance and see if investments like mutual funds, stock, ETFs, Index funds, Guaranteed Investments Certificate, Government Bonds are right for you.

- Be able to reassess your financial obligations: Upon further inspection of your financial plan you may see a liability that was not an issue in the past. But due to your current circumstances, they need to be addressed.

For example, looking through your finances, you may see that you should refinance your mortgage or restructure high-interest credit card debt to save on interest payments. Refinancing would improve your financial situation and leave more cash in your wallet.

Small actions like refinancing or consolidating your debt can make more sense the more you start to work on your finances.

- A Comprehensive Financial Planning Process in 7 Steps

- Financial Goals & Objectives – How To Set Financial Goals

- Financial Plans 101: What Are They and How Can You Make One?

-

- Drowning In Debt: The Definitive Guide To Debt Management & Paying Debt Off

- How does Consumer Credit Counseling Services Help to Tackle Credit Problems

- The Practical Guide to Purchasing Your First Investment Property

- Renting vs. Buying a House Debate: What’s Best For You?

Related: What Is Debt Consolidation Loan (Save More On Interest Payments)

How often should you make a financial plan?

Once you have compiled the perfect financial plan for your current financial needs and goals. It’s critical to revisit it at least once a year, at a minimum. Alternatively, if there is a big life-changing event that happens like you get a raise, get married, have a baby, or even buy a car. You should probably review and make proper adjustments and add them to your financial plan .

When big changes occur that affect your financial status (whether negatively or positively). You will probably want to create or adapt your current financial plan to accurately resemble your new financial standing.

It will do no good to stick with an old financial plan if it no longer represents your finances correctly. Like most things in life, your financial plan is a balancing act and will require flexibility as your life changes.

What’s the difference between a budget and a financial plan?

While you may think that budgeting and financial planning are the same thing. Matter of fact they do differ from each other even though there are similarities within the two. Budgeting focuses primarily on short-term goals and your finances “right here, right now.”

It is essential to focus on your immediate money issues. In addition to how you will spend your paycheck towards allocated categories. Ex: x% on bills, x% on retirement contributions, x% on entertainment, x% on groceries.

A financial plan, on the other hand, will utilize a budget to create a plan to achieve both long-term and short-term goals. A good budgeting plan can help you create a financial plan that is relevant to your daily life. However, in order to financially plan for your future, you will need a more in-depth financial plan, rather than just a budget.

Both budgeting and creating a financial plan are vital to your financial success, they both focus on different timelines for your money. Many financial plans often have some kind of budgeting built into the plan.

Related:How to Budget and Save Money (A Fresh Look at 6 Best Budgeting Methods)

Financial Plans: The best way to get control of your personal finances

One of the best things you can do for yourself, and for anyone that may depend on you, is to take control of your personal finances. We’ve covered a lot in this writeup and it can be overwhelming to someone who has never tried to attack this before.

But just remember that when the hard work is over, you will be much better off than you were before. Simply having the desire to learn more about managing your finances is a great step in the right direction!

You may also like the following posts:

What are your thoughts about the post? I would love to hear them in the comments below!

3 thoughts on “Financial Plans 101: What Are They and How Can You Make One?”

Pingback: How To Buy A Car At The Auction (Best Tips to help You Avoid Buying a Total Lemon) - Investadisor

Pingback: A Comprehensive Financial Planning Process in 7 Steps - Investadisor

Pingback: Rainy Day Funds: How Much Cash Should I Have on Hand - Investadisor